SPEI is Banco de México’s network that lets you send and receive money between bank accounts in real time, securely. Transfers are made via an app or online banking and generate an Electronic Payment Receipt (CEP) for tracking.

Looking for a way to move your money instantly from one account to another? Thanks to the digital SPEI system, backed by Banxico, you can. Whether you're paying for services, sending money to a relative, or making a big purchase.

This infrastructure is an essential tool for millions of people and businesses in Mexico. Still, some remain unsure about what SPEI is and how it helps make transfers more secure and efficient.

That’s why we’re here—to explain how SPEI works, its requirements, limits, and how to use it so you can make the most of your digital banking.

SPEI Transfer in Mexico: What It Is, How It Works, and Its Limits

What Is SPEI?

It’s the network developed by the Bank of Mexico to facilitate secure, real-time electronic payments. This system allows you to send and receive money instantly between bank accounts.

Of course, every SPEI bank transfer includes a behind-the-scenes settlement process between banks. Let’s take a closer look.

How Does SPEI Work?

The Interbank Electronic Payment System (SPEI) operates through online banking or a mobile app.

It starts when you log into your account and enter the recipient’s information, amount, and a payment concept. From there, the bank handles the rest:

The bank verifies that it’s really you making the transaction, using security measures such as passwords, SMS codes, or tokens.

Once confirmed, your bank structures the order securely and sends it to the Bank of Mexico through SPEI.

The SPEI system checks that everything is in order and, if so, transfers the funds to the recipient’s bank almost instantly.

The money lands in the recipient’s account within seconds, along with an official receipt: the Electronic Payment Receipt (CEP), which you can use to track the transfer or save for later.

SPEI is designed to operate every day of the year, 24/7, with total security and speed. That’s why it’s one of the most popular payment methods in the country.

What Do I Need to Use SPEI?

The requirements for making a wire transfer start with having an active account at a banking institution. In this case, you must also make sure that your bank offers the service.

Not all banks activate SPEI by default, so if it’s not available for you, request it.

Other requirements include:

Having the correct details of the person or company you want to send money to. This could be their CLABE (bank code), debit card number, or even a cellphone number linked to their account.

Registering the recipient’s account. In many cases, banks require you to add the recipient before making a transfer. Sometimes, you may need to wait a few hours or until the next day to proceed.

This makes it easier to manage personal finances and stay compliant with tax-related obligations.

How Much Money Can I Send Through SPEI?

SPEI transfer limits vary by bank. Each one sets its own rules, and these may differ based on the method used—mobile app, online banking, or branch.

It may also depend on the type of account you hold.

Here are maximum SPEI limits at some banks:

Bank

Method

Limit

CitiBanamex

Dimo (cellphone number)

8,000 MXN daily

BBVA

Branch, app, and online banking

Unlimited

Banorte

SPEI using cellphone number

11,500 MXN daily

Inbursa

Mobile SPEI with linked cellphone

1,500 UDIS daily / 4,000 UDIS monthly

Santander

Online banking, branch, and app

Classic and Preferred Customers: Up to $250,000 MXN

Select and Black customers: Up to $500,000 MXN

Private Banking Clients: Up to $1,000,000 MXN daily

Can I Change My SPEI Transfer Limit?

Yes, although options depend on your bank. Often, you can do this through their app or website, but some banks may require an in-person visit.

For example, BBVA and Santander allow you to increase limits online. In contrast, Citibanamex may require a branch visit depending on your account type.

Keep in mind, increases may be subject to security checks and may not take effect immediately.

A bank account with online or mobile banking access and an internet connection. Also, enough funds—via debit or credit card, depending on your bank.

Have one of these on hand:

CLABE (18 digits)

Card number (16 digits)

Linked cellphone number

Make sure the recipient's account is active.

2. Log in to your app or online banking

Go to your bank’s digital platform.

If you’ve never transferred to that account before, you’ll likely need to add the recipient first. Some banks allow immediate transfers, but others require a wait of up to 30 minutes.

3. Go to “Transfer” or “Send Money”

This section is usually within your main account view. Once you find it, tap:

Enter the amount

Enter the payment concept

Enter the reference number (you can set one of up to 7 digits or use the one auto-generated by the bank)

4. Verify and authorize the operation

Double-check all information and enter your security token or dynamic code if needed.

5. Save the payment receipt

Once done, your bank will provide a receipt with all the details. It will show the amount, date, receiving bank, recipient’s name, tracking code, reference, and payment concept.

Keep it in case you need to follow up.

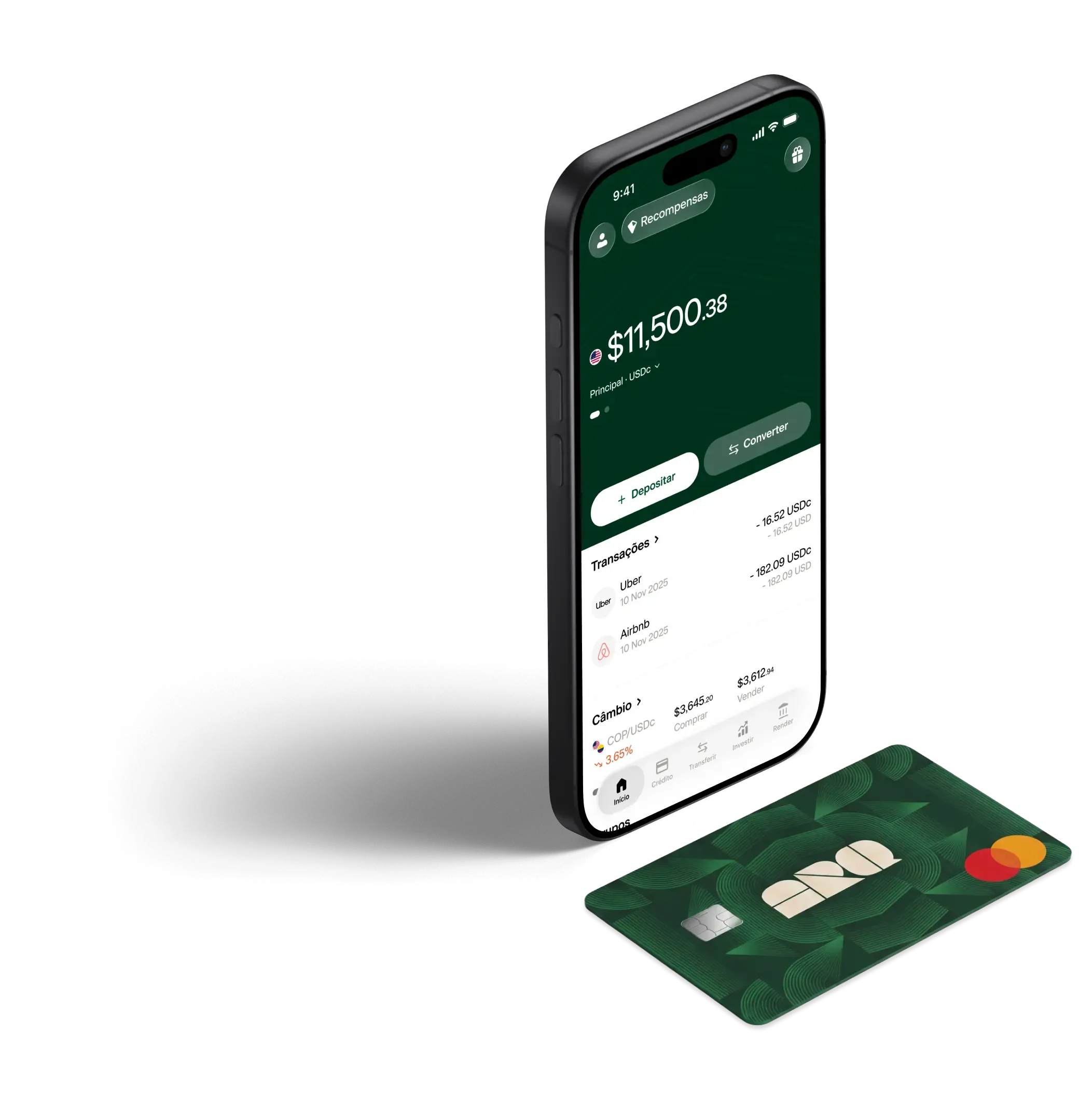

ARQ: A Practical Option for International Payments

If you need to send or receive money from abroad, try opening a digital dollar account with ARQ. It gives you total control of your funds with no maintenance fees and a clear interface.

The only fee you’ll pay is 3 USDc per transaction for sending or receiving digital dollars. You can also buy or sell USDc at a fair exchange rate, visible in real time right from the app.

If you're tired of bank fees or waiting days for a transfer, consider using ARQ. You won’t regret it.

Seu banco odiaria que você visse nossas taxas de conversão.

Converta dólares digitais e euros digitais em segundos, com as taxas reais do mercado. Sem taxas ocultas.